💲Valuation methodology

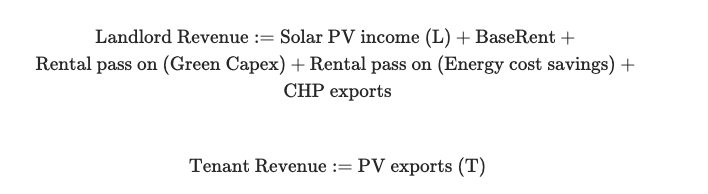

Revenues

- BaseRent: money coming from rent. Rent starts as the product of rentable area times base rent. It increases each year according to a formula that depends on the country/regulation. This formula takes into account:

- Rental pass on Green Capex: Fraction of Green Capex that leads to an improved primary energy demand of the asset

- Pass-on rate: Fraction of modernization (or “green”) Capex that is passed on as an annual rent increase

- Pass-on cap: Maximum rent increase per square meter and year resulting from modernization Capex.

- Cap horizon (years): Defines the rolling time period over which the specified pass-on cap applies. If multiple modernization measures occur within this horizon, their cost pass-ons are aggregated to ensure that the pass-on cap is not exceeded within the defined window.

- Zones: Selection of zones on which the Capex can be passed on.

- Rental pass on Energy costs savings: Fraction of annual energy cost savings that is passed on as annual rent increase.

- Solar PV income / CHP Exports (L): Money received from energy providers when dumping unused energy into the network or from tenants when selling it in-house for self-consumption.

- PV Exports (T): Only under specific PV contract conditions, where the net income of PV is not flowing to the landlord but the tenant.

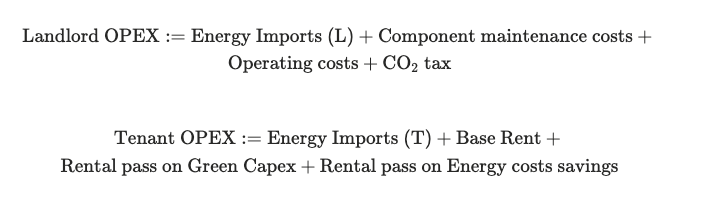

Operating costs: OPEX

- Energy imports: Money paid by landlord or tenant to providers for energy.

- Component maintenance costs: Money spent maintaining components supported by Optiml

- Operating costs: Annually recurring operating costs that are always paid by the landlord. They can be onboarded via Asset Edit.

- CO2 tax: Money spent for consuming fossil fuels (Gas/Oil) on site.

Other:

- Accounting-wise, OPEX also takes into account depreciation and interest costs. Note that we track depreciation separately and we don’t consider interest costs. Outside of OPTIML, this definition would usually be called Cash Operating Expenses and tracked in the Operating Cash Flow statement.

- Depreciation: This is relevant for NI and valuation. It is defined as the annualized capital expenditures of installed components.

- Note that our depreciation is different from accounting depreciation.

- If a system is replaced before the end of the lifetime, the remaining non depreciated asset is lost and not considered available for depreciation anymore.

- Additionally, we consider scaffolding when depreciating some envelope components even though it is a non capitalizing expense. We do this for valuation purposes.

- Note that our depreciation is different from accounting depreciation.

Capital expenditures: CAPEX

- Component investment costs: investment costs resulting from renovating/replacing system, interior or envelope components.

- Scaffolding costs: costs resulting from renovating the facade. It is tracked separately because it usually cannot be capitalized or passed on to rent. We include it in the depreciation for valuation purposes.

- Planning costs + Risk margin: Extra costs set with a multiple in asset strategy development.

- Capital expenditures are always paid by the landlord.

Total cost for the optimization:

- This is the function that we optimize for in the “Min cost” optimization.

- Total cost := OPEX (L+T) + CAPEX(L) - Solar PV Income from grid exports - CHP exports

- Note that it has some revenue components but it is missing some like the rent income.

Cashflow Reporting

- NOI: Net operating income := Revenue (L) - OPEX (L)

- NI: Net income := Revenue (L) - OPEX (L) - Depreciation (L)

- NCF: Net Cashflow := Revenue (L) - OPEX (L) - CAPEX (L)

- Total cost := OPEX (L) + CAPEX(L) - Solar PV Income (L) - CHP exports (L)

Green Capex

Green Capex is the portion of capital expenditure that directly contributes to a measurable reduction in Primary Energy Demand (PED), Energy Use Intensity (EUI), or carbon emissions, relative to a hypothetical replacement of the component.

Examples:

- Facade:

- Facade EOL with lower PED/EUI= 700'000 € incl. Scaffolding/planning/risk etc.

- Facade EOL with same PED/EUI = 500'000 € incl. Scaffolding/planning/risk etc.

- Green Capex = 200'000 €

- Scaffolding happens in any case and is never green

- Solar PV (kWp) (& battery in kWh)

- The delta of the EOL PV replacement and a potential PV kWp increase, if it leads to PED reduction:

- PV old: e.g 20 kWp EOL at certain PED due to self consumption = 40'000 €

- PV new: e.g. 30 kWp EOL at lower PED due to self consumption = 50'000 €

- Green Capex = 10'000 €

- Lighting/Appliances/Energy saving measures (BMS, sensors, tenant education, smart thermostats)

- 100% green Capex if it reduces PED

- HVAC systems

- HVAC system old with same PED = 300'000 €

- HVAC system new with lower PED = 400'000 €

- Green Capex = 100'000 €

- Additionally for green Capex, we add the additional constraint that the new system cannot be a fossil based system.

- Hot water tank/Buffer tank:

- Never green Capex

- HVAC outputs:

- Never green Capex

- Solar thermal:

- 100% green Capex if it reduces PED

Valuation methods

These are the two methods that we might use. Unless stated otherwise, market value uses the first method (Exit perpetuity).

Note that our optimization works with a single discount rate that can be set by the user as well in Asset Edit. The valuation computation happens after the optimization of measures is done.

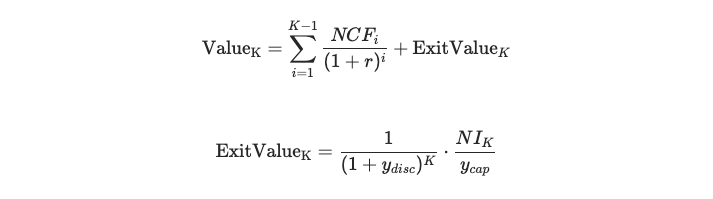

Valuation (via Exit Perpetuity):

The asset is valued as a financial asset that gives a certain cashflow until the end of time. If the discounting value is positive, the resulting series is converging to the following valuation:

- r: discount rate holding period (%)

- y_disc: Discount rate exit (%)

- y_cap: Exit cap rate (%)

- K: exit year

- Note that this valuation does only include cashflows until year K.

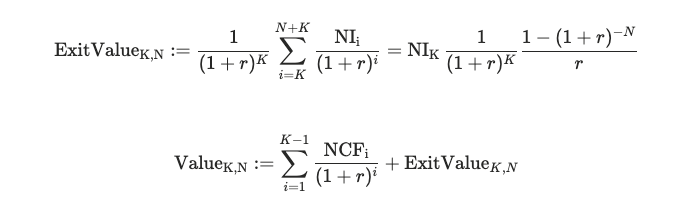

Valuation (via Exit Annuity):

The asset is valued at exit point K as the sum of the N future cashflows (K year onward) discounted to the present plus the the cashflows from year 1 to K.

- r: discount rate

- K: exit

- N: horizon

- For example, we typically use the 90 year, 10 exit annuity valuation, which is the valuation in 10 years of the 90 consequent cashflows discounted to the present.

- The formula equivalence assumes that NI stays constant after year K.

- ExitAnnuity valuation is the same as ExitPerpetuity valuation for big values of N.

ROI metrics

- Net ROI rate: Net operating income yield measures how valuable is a given asset. The net ROI is computed for the cashflows of the landlord (L).

- As value, we can use any of the previous valuation methods or the market value if available.

- Gross ROI rate: gross return on investment. Measures yield before any cost.

- Cashflow ROI rate (after renovation): net return on investment after renovation or CAPEX. Measures yield after all costs. Abnormally low on high CAPEX years. An average over a period should be used to compare.

IRR metrics

Asset-level IRR

- Purchase Price: Asset purchase price.

- All cashflows are from a Landlords perspective.

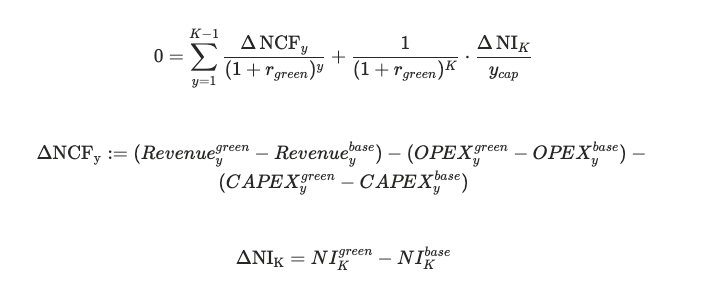

Green measures IRR

- Green Capex: Fraction of Capex that is considered Green as per methodology.

- Revenue (green/base): Revenue of the strategy with green measures or the baseline strategy without green measures.

- OPEX (Green/base): Opex of the strategy with green measures or the baseline strategy without green measures.

- Capex (Green/base): Capex of the strategy with green measures (“Green Strategy”) or the baseline strategy (“Not-Green Baseline”) without green measures. The baseline is not the “BASELINE” tagged strategy, it is a unique “Not-Green Baseline” strategy just for the computation of the Green IRR, that is not exposed to users. Below you will find examples of how we compute the Green IRR depending on the component replacement

- Baseline Examples:

- Facade: Current facade (what’s currently in the building). U-value: 0.2

- “Green Strategy”: Facade retrofit. U-value: 0.1, retrofit year: 2030

- “Not-Green Baseline”: Facade retrofit. U-value: 0.2. retrofit year: 2030.

- Closest u-value to current, representing a replacement with itself, that does not affect PED, EUI or CO2.

- Same year as green strategy.

- We compute a theoretical “Not-Green Baseline”: that represents: What if I just replace the current component with itself in the year that the green strategy defines.

- Any envelope component is treated in the same way.

- PV: Current: 10 kWp.

- “Green Strategy”: Retrofit & Increase: 20 kWp. Year: 2030.

- “Not-Green Baseline”: Replacement: 10 kWp at end of life 2040.

- HVAC: Current: Gas Boiler (10kW) + Absorption Chiller (10 kW)

- Green Strategy: Reversible Air Source Heat Pump (15 kW) in 2030

- e.g. due to better u-value you can install a smaller system

- “Not-Green Baseline”: Replacement Gas Boiler (10kW) + Absorption Chiller (10 kW) at end of life 2040

- Green Strategy: Reversible Air Source Heat Pump (15 kW) in 2030

- Lighting/Appliances/Energy saving measures:

- “Green Strategy”: Maybe installs the new lighting

- “Not-Green Baseline”: Keeps current system, but no end of life Capex, as we do not yet have data that represents older systems that are no longer in use. This is a known limitation to the methodology.

- Note: In case the asset has already the newest systems installed already, both strategies will just keep the systems in place. The IRR will be undefined. This holds true for any replacement in which the old and the new system are identical.

- Facade: Current facade (what’s currently in the building). U-value: 0.2

- Baseline Examples: